Whether renting or buying homes, Australians face greater challenges this year as housing affordability plummets. The ANZ CoreLogic Housing Affordability Report from April 2024 outlines the state of Australia’s housing and rental markets.

Due to the rapid rise of housing costs, the portion of median income needed to service rents has increased significantly. This historic increase will strongly impact Aussie renters and their ability to maintain stable housing.

Borrowing capacity has also decreased, as homeowners face sharp increases in mortgage rates. Prospective buyers, especially first-time homeowners, are most affected as borrowing costs soar.

Rental Market Challenges

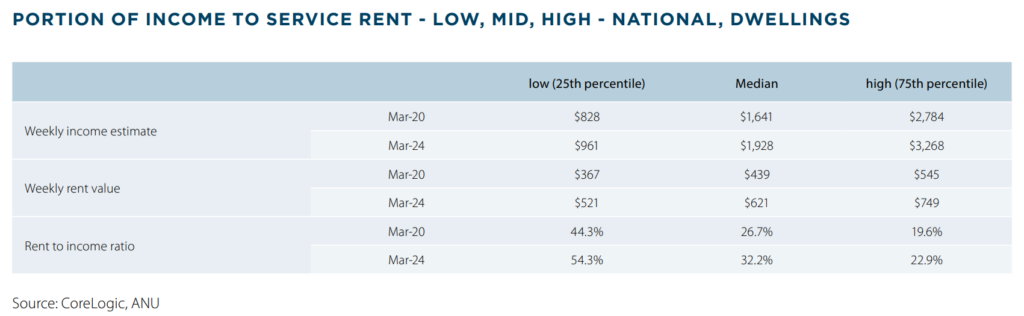

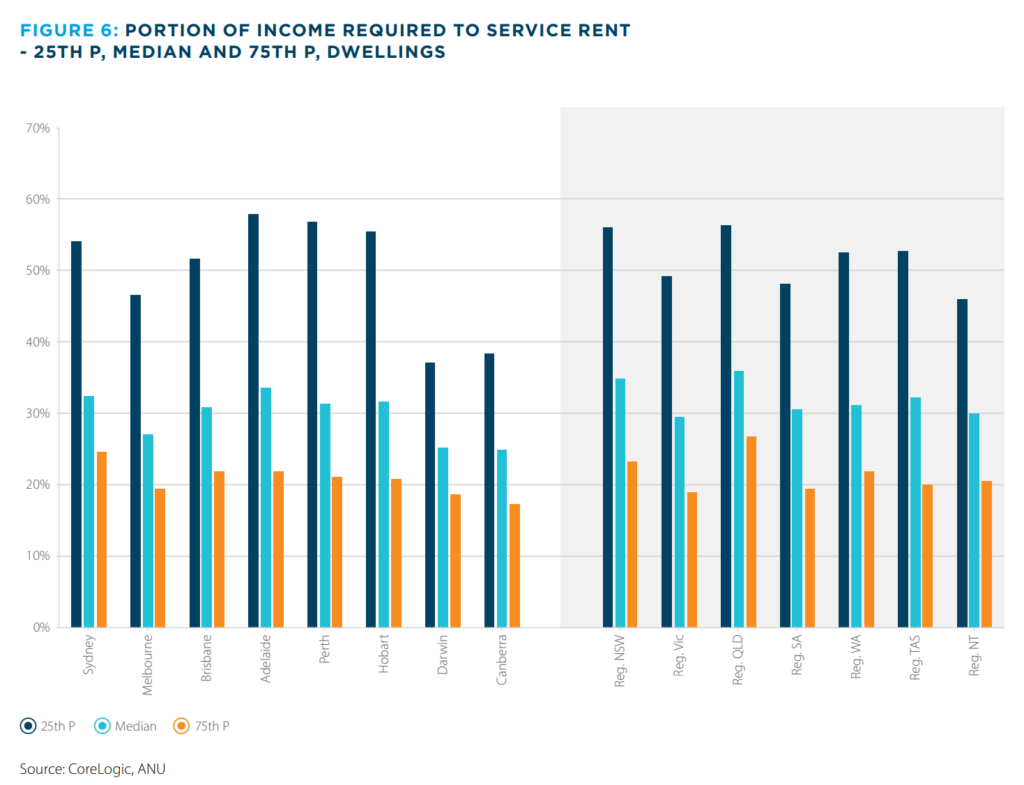

The portion of income needed for median new rents hit a record high of 32.2% in March 2024, up from the mid-20% range in previous years. Spending above 30% of income on rent can leave little funds for other essential costs, like other debt obligations and household expenses.

Low-income earners are those most affected by the declining affordability of housing as the cost of rent now consumes 54.3% of their already strained incomes.

This record increase invalidates the benefits of the higher minimum wage hikes in recent years. The Fair Work Commission increased the minimum wage by 5.75% in 2023, which is a $48 increase for the weekly pay of full-time workers. This is almost equivalent to the $53 increase in rent prices for those in the 25th percentile. Even with wage increases, housing remains out of reach for those with low income.

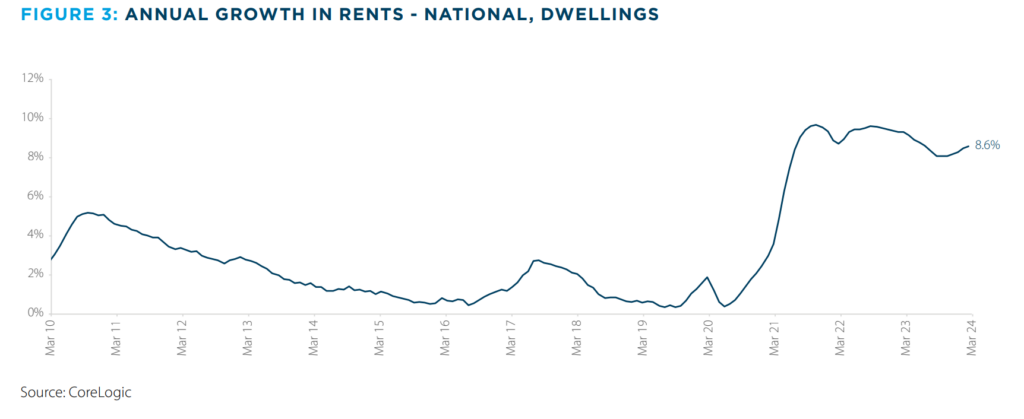

At the start of 2024, rental prices started to increase again after a period of slower growth. The increase has risen to 8.6% from October 2023’s 8.1%. This increase was especially noticeable for house rental prices, which were at their lowest at 6.8% in September 2023. By March 2024, this rate had increased to 8.4%.

Mortgage Affordability

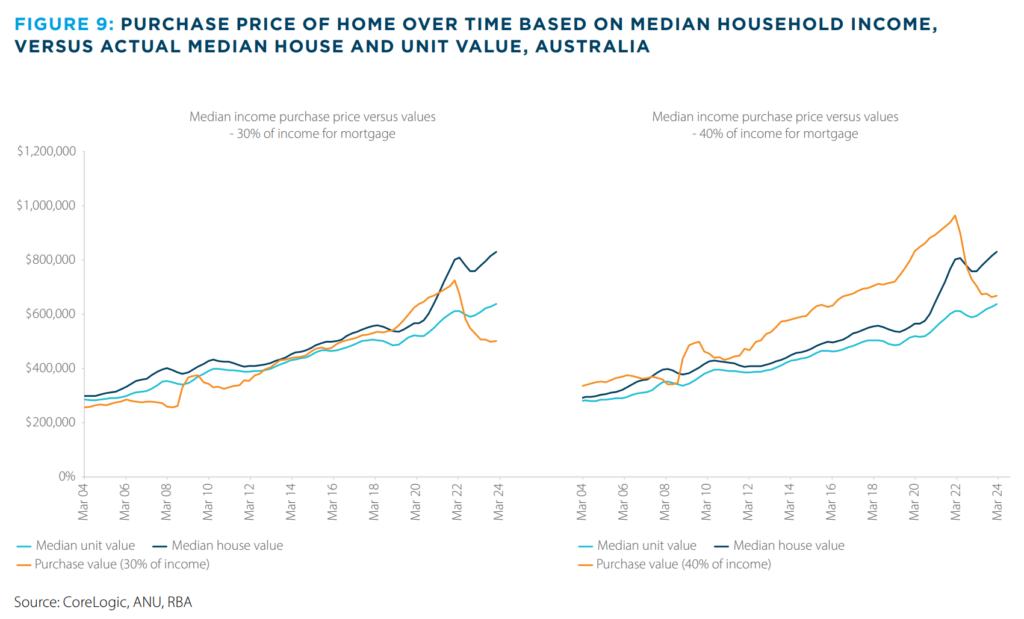

Borrowing capacity has also decreased amid rapid increases in the RBA’s cash rate targets. If a prospective home buyer earns around Australia’s median income, spending 30% on mortgage payments means they can afford a home worth $503,000. However, the median unit price is $640,000, while the median house price is $834,000.

For median-income earners to afford the median unit price, they will have to allocate 40% or more of their income to mortgage repayments, which can seriously strain their finances.

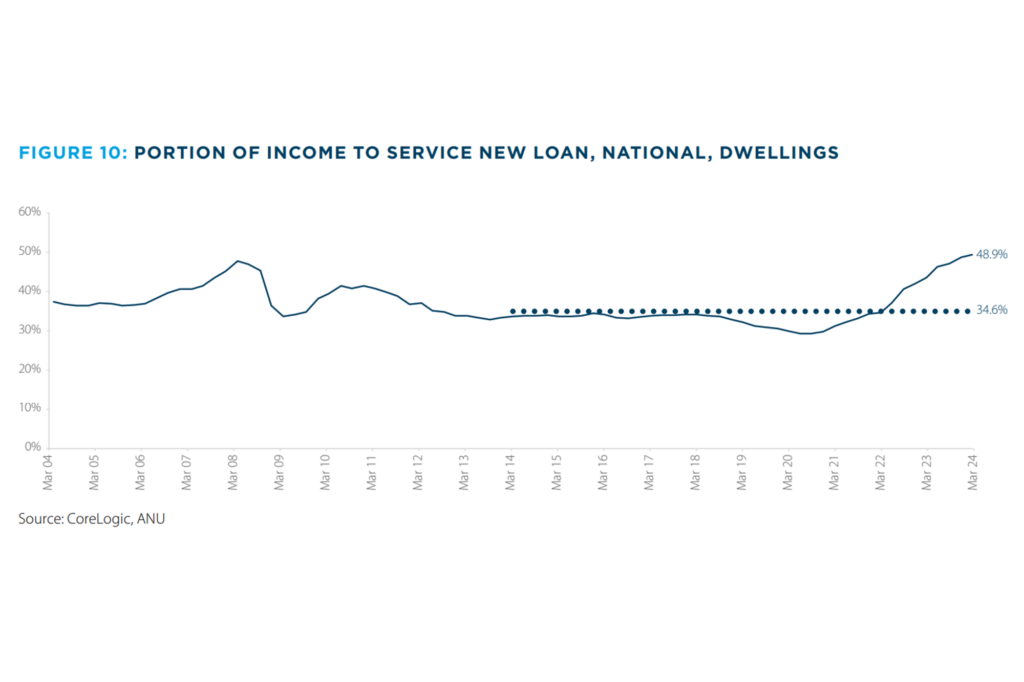

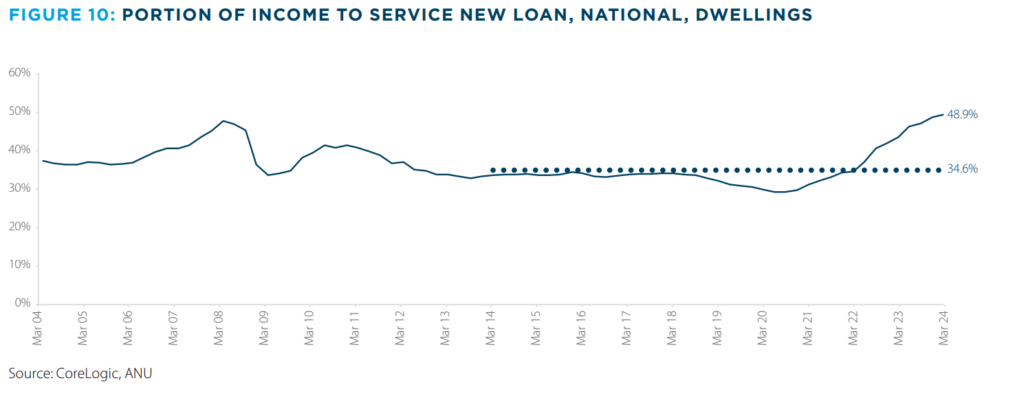

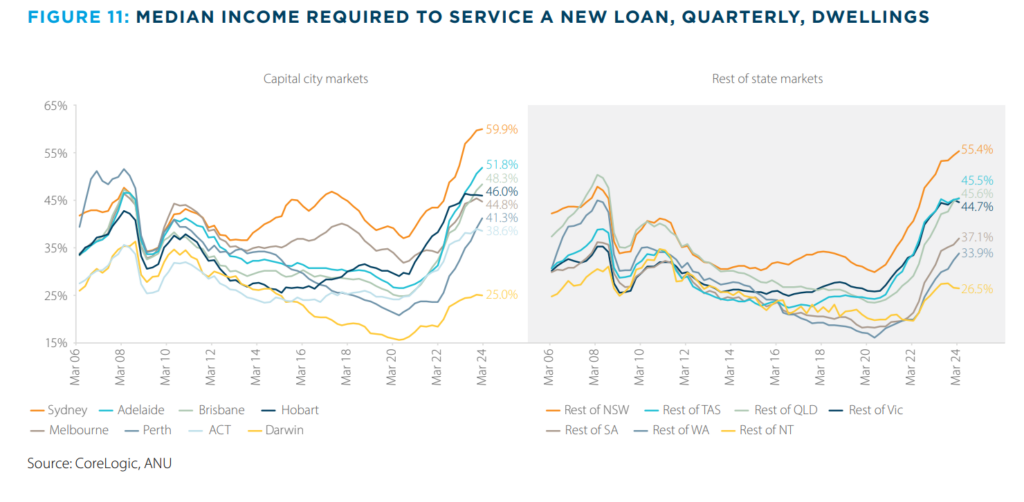

The portion of median income needed to service a new loan has now reached 48.9%, a high jump from the last decade’s 34.6%. This is due to home values reaching record highs and the cash rate rising 25 basis points.

The record-high portion of 48.9% isn’t something many median-income households will have to pay. However, the figures skyrocketing to this amount reinforces how Australians’ current income isn’t enough to catch up to rising interest rates.

Regional Disparities

The report highlights significant regional variations in affordability. For example, Adelaide and regional Queensland exhibit some of the highest rent-to-income ratios.

In contrast, places like Darwin and Canberra have relatively lower ratios, suggesting slightly better affordability in these areas.

Meanwhile, the portion of median income required to service a new loan on a median Sydney dwelling is significantly higher than in regional areas of NSW. This pattern of higher mortgage serviceability requirements in capital cities as compared to regional areas is consistent across Australia.

These regional disparities highlight the uneven burden of housing costs across Australia, with some areas facing far more pronounced affordability issues than others.

The Need for Policy Interventions

There is a growing focus on rental market reform in public policy due to worsening affordability. Proposed changes include establishing consistent national standards for rental evictions, improvements to rental standards, and limits on rent increase frequency. On the supply side, there are efforts to meet ambitious housing targets and increase the provision of social and affordable housing through various government initiatives and incentives.

In Summary

The report paints a concerning picture of housing affordability in Australia, with significant challenges for renters and prospective homebuyers, particularly those with lower incomes.

It calls for continued and enhanced policy intervention to address these growing affordability issues.

Adjusting Your Mortgage Amidst Rising Borrowing Costs

For those currently paying off their mortgages, it’s important to know all avenues to cope with the rising interest rates. Some may increase their earnings and tighten their budgets to accommodate the higher mortgage payments. However, if payments are taking the lion’s share of your income, it’s worth considering loan adjustments. Refinancing, restructuring, or consolidating debts may help ease the burden of deteriorating housing affordability.

If you want to modify your mortgage, don’t hesitate to reach out to loan experts to guide you.